Posted on Wednesday, August 24, 2022

Posted on Wednesday, August 24, 2022Zoom Video Communications, Inc. recently filed suit against four of its insurers alleging that it is owed their policy limits due to paying over $90 million in litigation costs stemming from several underlying lawsuits -- a government investigation and subsequent lawsuit and several other private lawsuits. All of the underlying lawsuits claimed data security breaches and consumer protection violations against the company. Zoom argues that the insurers wrongfully denied coverage for these lawsuits by improperly relying on “loose” interrelated acts language in their policies.

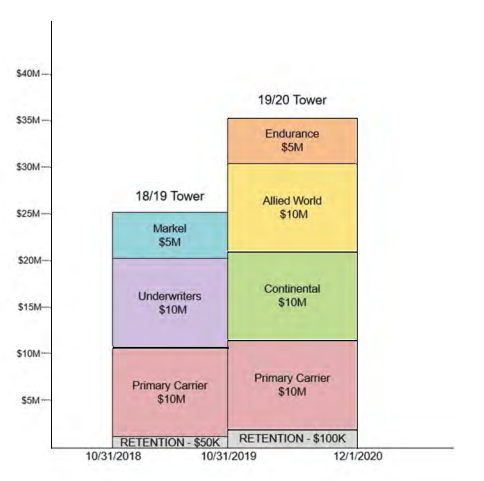

After the underlying lawsuits were settled, Zoom sought reimbursement from its excess insurance policies, implicating the excess policies within two separate errors and omissions cyber insurance “towers.” Each tower covered a specific policy period (18/19 and 19/20, as per the diagram below) and the various lawsuits were filed during both periods, with the government’s investigation and lawsuit filed in the first tower’s policy period along with a consumer watchdog lawsuit. The other private lawsuits were filed during the second tower’s policy period.

After Zoom sought recovery from both towers, the carriers began playing what amounted to musical chairs, pointing their fingers at each other, hoping that the last one standing would be ultimately responsible. Specifically, the carriers in the second tower with the 19/20 policy period argued that they were not responsible because the lawsuits that arose during its policy period were “related to” or arose out of the same incident or interrelated incidents in the initial government investigation headed by the Federal Trade Commission (FTC) that began under the first tower and the 18/19 policy period. Therefore, the carriers for the second tower argued that all the lawsuits that arose during the second tower policy period should be included under one, initial claim and covered under the first tower.

The first tower carriers denied excess coverage for the FTC lawsuit and watchdog lawsuit that arose during its policy period, even though Zoom’s primary carrier under the first tower agreed to cover the claims. The first tower excess carriers denied the claims arguing that the FTC investigation was not a covered claim and, even if it was, the FTC claim and the consumer action lawsuit were both subject to exclusions, including the False Advertising and Antitrust Exclusions.

The first tower excess carrier also denied coverage for the private lawsuits because they arose during the second tower policy period. Further, the first tower excess carrier claimed that the later lawsuits were not “related to” nor did they arise out of the same incident or interrelated incidents as the FTC investigation and, therefore, not covered under the first tower excess policy.

The foregoing information was taken from Zoom’s complaint only. We do not yet have copies of the excess carriers’ response to Zoom’s lawsuit.

Everything is Everything

The Zoom case highlights the danger to policyholders when it comes to related claims denials because, when pushed to the extreme, everything is related to everything to some degree. The facts as outlined in the Zoom complaint are evidence of an increase over the last several years of carriers using ambiguous and “loose” interrelatedness clauses in policies to deny coverage. These clauses allow insurance companies to basically claim whatever they want, depending upon their particular interests in a factual scenario.

Because the relatedness language in policies is so malleable, one can make the argument that even clearly unrelated claims that arose during different policy periods can, in some way, be related. There appears to be no bright-line test in determining whether claims are related, making it difficult for courts and turning every case involving a relatedness denial into a highly fact-based analysis.

This issue relates to an article I wrote in May 2021 entitled, “Multiple Claims” Provisions on Contractor’s Professional Liability Policy Creates a Trap for Policyholders, where I outlined a potential trap for policyholders when there is an untimely notice of claim. The article discussed the case of Berkley Assurance Company v. Hunt Construction Group, Inc., 465 F.Supp.3d 370 (S.D.N.Y. 2020), where the court upheld an untimely notice of claim denial from the contractor, then also upheld the denial of the owner’s claim due to it being “related to” the contractor’s claim that was deemed untimely.

In the article, one of the arguments made was that when policyholders have a claim, they will now not only have to consider coverage for that claim but must also consider that failing to give timely notice may jeopardize coverage for unknown future claims that may be deemed to be “related.” Policyholders can no longer risk waiting to provide notice of a claim or potential claim, even if that claim may fall within a deductible or retention. To preserve coverage for future claims, policyholders must give notice of anything that may qualify as a claim.

With insurance companies increasing the use of “flexible” interrelatedness clauses, policyholders need to be even more vigilant not to fall into these traps.

For more information, contact Michael V. Pepe at MPepe@sdvlaw.com.