Posted on Tuesday, April 16, 2019

Posted on Tuesday, April 16, 2019

Project-Specific Commercial General Liability Insurance - Understanding Repair Work Endorsements

by Jeremiah Welch

Many markets which provide insurance for construction projects include an endorsement providing coverage for “repair work” as part of their standard policy. “Repair work” endorsements are largely misunderstood by policyholders and the insurance broker community. They are typically assumed to be coverage enhancements, but many provide no additional coverage and actually risk reduction of coverage otherwise provided as part of the products-completed operations (“PCO”) extensions also found in these project-specific policies. This article is designed to help the reader understand these endorsements so that better decisions can be made at the point of purchase.

Intent

The common feature of these endorsements is a grant of coverage for bodily injury and property damage resulting from “repair work” for a specified period of time. Most endorsements define “repair work” to mean the repair of completed work performed pursuant to a contract or warranty.

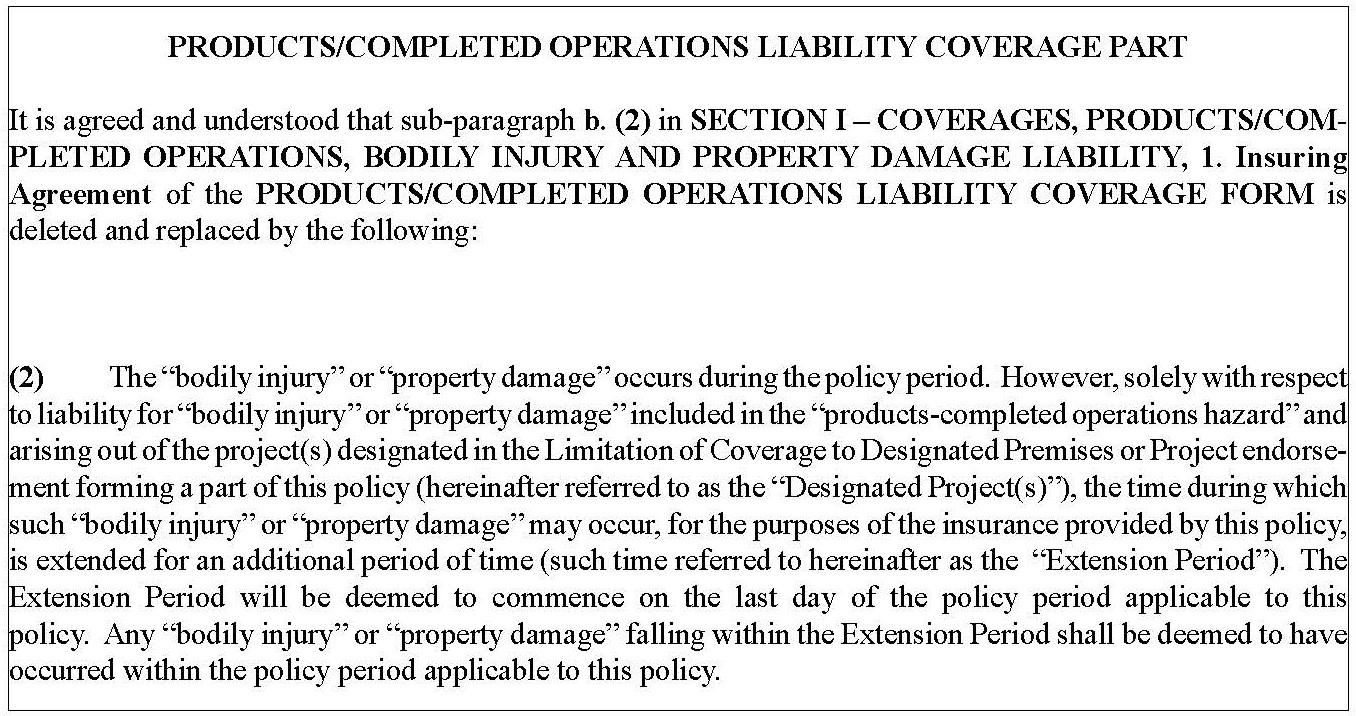

The following is an example of a repair work endorsement used by a leading excess and surplus lines insurer:

.jpg)

In short, the PCO hazard applies to completed work. There are two parts of the definition that are critically important to understanding how it can conflict with the typical repair work endorsement. First, the definition states that PCO includes all bodily injury and property damage which “arises out of” your product and your work. In disputes about policy interpretation, the courts have consistently interpreted the phrase “arising out of” to mean any connection or relationship. “Arising out of” does not mean a direct (or “proximate”) causal connection. The second significant piece of the definition is the clarification at the end, which states that “work that may need service, maintenance, correction, repair or replacement, but which is otherwise complete, will be treated as completed”. When a policy grants an extension of coverage for the PCO hazard, it grants coverage for bodily injury and property damage arising out of the repair of completed work.

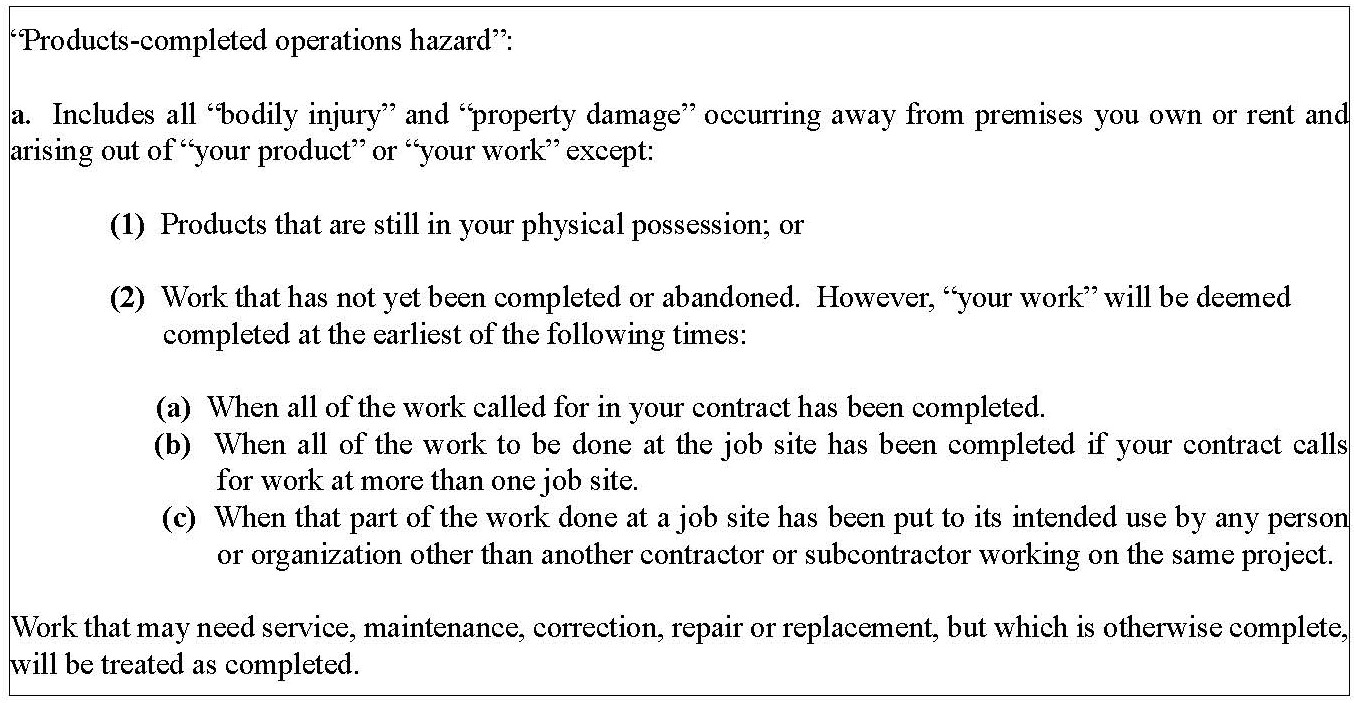

Now, compare this to the definition of “repair work”, for which coverage is granted via the repair work endorsement example above:

In this example, the repair work endorsement is granting coverage that is already present in the policy through the PCO extension. But, note that the repair work endorsement also includes the following provision:

The endorsement does not explain how to reconcile the inconsistency between this statement and the fact that the PCO extension already includes coverage for repair work. Now consider the fact that most PCO extensions provide coverage to the applicable statute of repose or 10 years, whereas most repair work endorsements provide an extension of only 2 years.2 The courts have yet to tackle this issue. The risk here is that an insurer having issued a policy including both a repair work endorsement and a PCO extension, would argue that claims for injury or damage arising out of repair work are covered only for the period of time specified in the repair work endorsement.3 The argument would be that the repair work endorsement carved out a subset of the PCO hazard and limited its coverage period to the time specified in the repair work endorsement. In the typical policy, this means that coverage for injuries or damage arising out of repair work is reduced from 10 years to 2 years.

Do Repair Work Endorsements Offer Any Benefit?

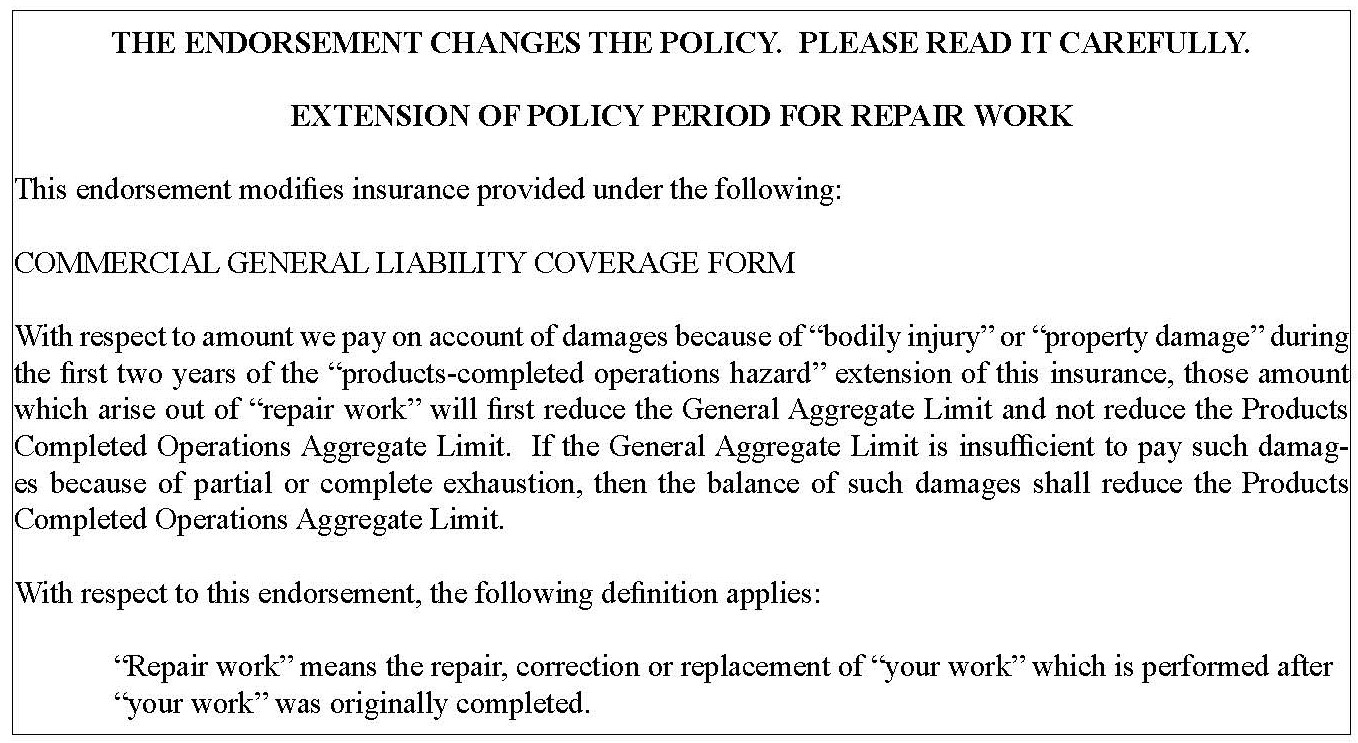

There are many different permutations of “repair work endorsements”. These are manuscript forms used for a risk that is heavily underwritten by excess and surplus lines insurers. As such, these forms are typically not filed and can be freely changed year-to-year and placement to placement. Most forms do suffer from the challenge outlined above, however there are a few that do not. A small subset of “repair work endorsements” simply state that any “property damage” resulting from “repair work”, within the set time period, reduces the policy’s general aggregate limit, not the products-completed operations limit. The following is an example:

Note that this endorsement does not include the troublesome statement that “repair work” does not apply to “bodily injury” or “property damage” in the “products-completed operations hazard”. Nor does it support an argument that “repair work” coverage is limited to two years; the only change is that for two years, “repair work” otherwise covered by the “products-completed operations extension” counts first against the general aggregate limit. This language could easily be combined with the “products-completed operations extension” language/endorsement of the policy. An endorsement such as the above is a desirable enhancement. The intent here is to use the general aggregate limits remaining at the end of the policy period to pay claims arising out of “repair work” (what the industry would typically refer to as “call-back” or warranty work), thereby preserving the products-completed operations limits for more traditional construction defect claims.4

“Repair work” endorsements require careful scrutiny, armed with the knowledge that most market offerings are at best redundant and at worst restrictive of coverage otherwise available under the “products-completed operations extension”. When negotiating coverage, care should be taken to avoid problematic endorsements, and, if possible, replace them with something akin the above example which addresses only the transfer of “repair work” risk to the general aggregate limit.

For more information please contact Jeremiah Welch at 951-365-3147 or jmw@sdvlaw.com.

_________________________________________________

1 The point about the “grant of coverage” for the PCO hazard is important. In the standard ISO form policy, the PCO hazard is a defined term which is referenced in the policy for two primary reasons: (1) to frame the circumstances under which a specific set of limits (the PCO limits) apply, and (2) to describe the conditions under which exceptions to certain exclusions apply. The coverage grant of the ISO policy does not distinguish between ongoing and completed work. Because the project-specific policy is not an annually renewing “practice policy”, but must still account for liability on completed work, most of these policies include a specific grant of coverage for the PCO hazard for a period of time following completion of the project.

2 Most PCO extensions are designed to provide PCO coverage to the applicable statute of repose, so that the builders and contractors have coverage for their statutory liability period.

3 According to the rules of insurance policy interpretation used by most courts, more specific language controls over general language. Courts usually apply the principle of “in pare materia”, meaning that one looks for a plain meaning interpretation whereby all the provisions of the policy can be applied without inconsistency. Here, it is not inconsistent to read the “repair work endorsement” as a more specific treatment of a specific subset of the work covered by the “products-completed operations extension”, with a shorter coverage period. Our fear is that common principles of policy interpretation will result in the typical “repair work endorsement” limiting the coverage that would otherwise have been available under the typical “products-completed operations extension”.

4 Note that whether covered under a “repair work endorsement” or a “products-completed operations extension”, the claim must still allege “property damage” caused by an occurrence, which most states interpret to include physical injury to tangible property resulting from defective work. To date, no states have found an “occurrence” and “property damage” where there is only defective work and no resulting damage.

Click on this link to view the article in pdf format